Hello. This is Stanton Jones and Steve Hall with what’s important in the IT and business services industry this week.

If someone forwarded you this briefing, consider subscribing here.

Solid Q1, but Uncertainty Ahead

The IT and business services industry continued to show resilience in Q1 despite macro-economic uncertainty. Sweeping tariffs and potential retaliatory measures are further intensifying short-term uncertainty, especially related to discretionary IT spending.

Data Watch

1Q25 Recap

- Managed services annual contract value (ACV) was up 2% Y/Y.

- EMEA led the growth in managed services; Americas was flat.

- BFSI was down 2% but showed signs of recovery over the last six months.

- ITO posted solid growth in both applications and infrastructure.

- Broad-based weakness in BPO spanned all service lines.

- Six mega deals (ACV > $100M) were awarded, up from four in 1Q24.

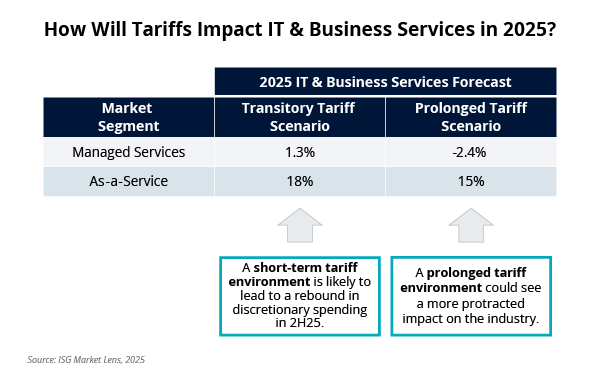

2025 Forecast

Despite a solid Q1, heightened uncertainty from trade policy, geopolitical tensions and evolving regulations is beginning to weigh on second-quarter forecasts. Enterprises are in a wait-and-see mode, holding discretionary budgets and re-evaluating capital-intensive projects.

Given the uncertainty in the environment, we’re providing a scenario-based approach for our full-year outlook:

- Scenario #1: If tariffs are short term, we expect to see a rebound of discretionary spending in 2H25. In this scenario, we’re forecasting managed services to grow 1.3% and as-a-service to grow by 18%.

- Scenario #2: If tariffs cause a more protracted impact on the industry, we expect to see −2.4% growth for managed services and 15% growth for as-a-service.

You can catch a replay of the call here and download the slides here.

About the authors

Stanton Jones

Stanton helps enterprise technology leaders, IT service providers and buy- and sell-side professionals make sense of the global IT services sector. Stanton's weekly briefing - the Index Insider - is read by thousands of industry stakeholders each week.

Steve Hall

Steve Hall is Chief AI Officer, leading the firm’s work to help clients create an AI strategy, select the right business partners and deliver meaningful value and outcomes. His industry-leading expertise in navigating the complexities of adopting technology at scale is helping both clients and ISG leverage AI to drive value into every aspect of their operations. Steve joined ISG in 2005 and has led ISG Digital Advisory Services, Emerging Technology Services, Global Product Engineering and Application Development & Maintenance. Trained as a software engineer, he serves on the Advisory Board of Consortium for Information & Software Quality (CISQ). He holds a bachelor’s degree in computer science from Regis University.