Hello. This is David Lessin standing in for Stanton Jones with what’s important in the IT and business services industry this week.

If someone forwarded you this briefing, consider subscribing here.

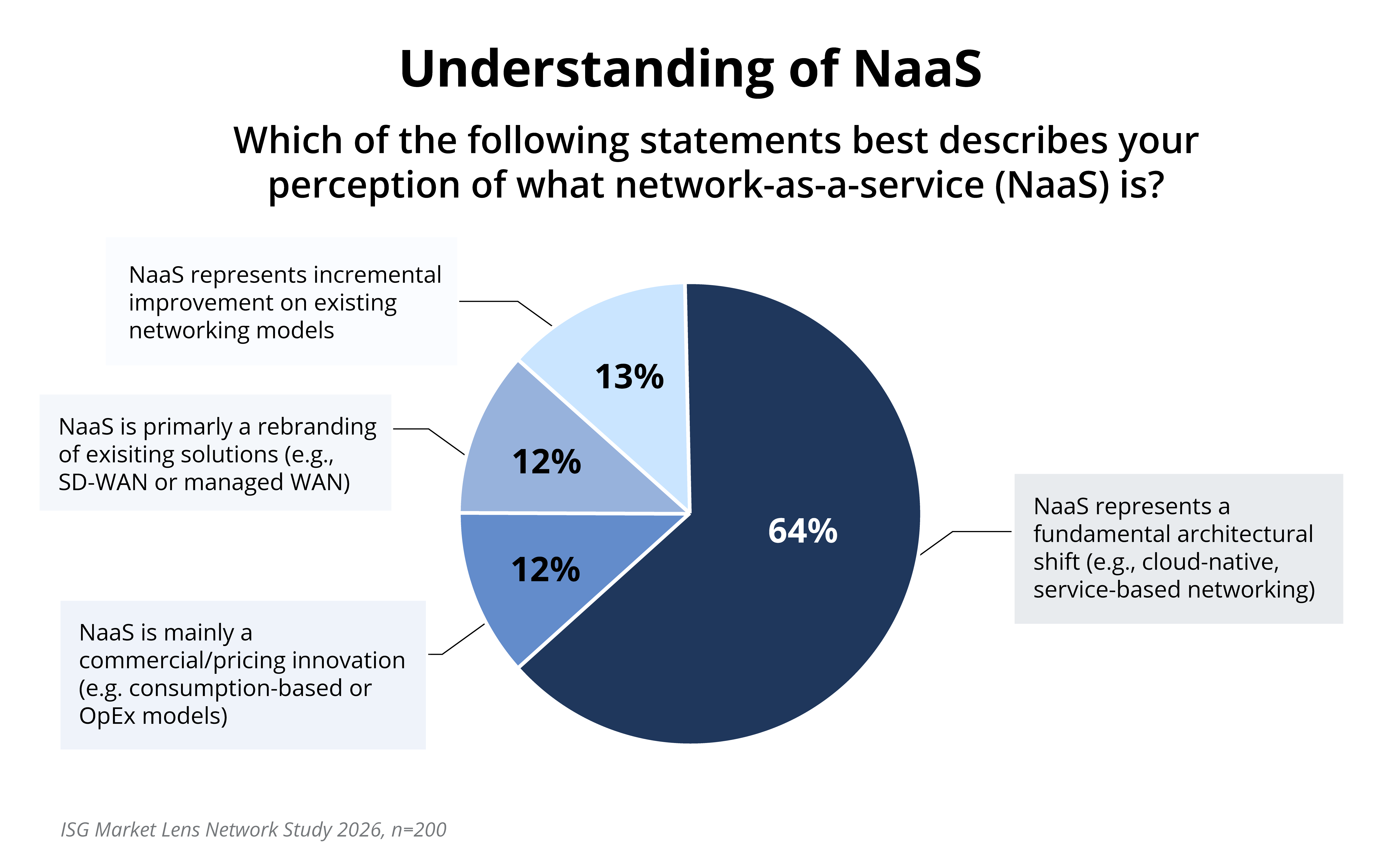

Understanding NaaS

The ISG Market Lens 2026 Network report provides interesting findings on how enterprises perceive network-as-a-service (NaaS). While the report clearly shows enterprise interest in NaaS is strong, the data also signals a lack of understanding about the two distinct types of NaaS providers.

Data Watch

Background

Given the continued interest in NaaS from both enterprise and provider communities, we wanted to better understand the details around NaaS adoption and enterprise attitudes. We conducted a study of enterprise customers, polling their knowledge, sentiments and outlook about NaaS.

The Details

- 64% of respondents believe NaaS represents a fundamental architectural shift.

- 13% of respondents believe NaaS represents an incremental improvement on existing network models

- 12% of respondents believe NaaS represents a rebranding of existing solutions (e.g., SD-WAN or managed WAN).

- 12% of respondents believe NaaS is mainly a commercial/pricing innovation (e.g., consumption-based or OpEx models)

Why It’s Happening

At a high level, the NaaS provider market can be split into two wide categories: 1) the dominant hyperscalers/cloud providers and 2) more recently available carrier transport providers. The former specializes in hosting workloads; the latter specializes in connecting the workloads. Both types of NaaS providers are driving consumption models that target different areas of the enterprise technology stack. Enterprises that don’t have a clear understanding of the capabilities of each could see value leakage.

If NaaS providers improve communication to enterprise stakeholders across the technology stack – articulating where their respective NaaS solutions add value and, more specifically, where they do not – enterprises will find these solutions do, in fact, bring more value.

Hyperscalers/cloud providers and underlay providers are not natural competitors. In fact, we see them as natural partners. By working in partnership with each other and the enterprise, NaaS providers can drive partial adoptions through transition, reaching more fully transformed enterprise goals.

In our view, an enterprise should capitalize on both types of NaaS providers and create win-win-wins for all parties. Carrier NaaS transport providers can help enterprises avoid vendor lock-in, enable workload migrations and provide connectivity at the edge, while hyperscaler and cloud providers can provide the infrastructure for the apps and AI workloads. This is especially critical as the carrier NaaS providers are actively releasing new features to help enterprises realize more value from their cloud workloads.