Hello. This is Michael Dornan with what’s important in the IT and business services industry this week.

If someone forwarded you this briefing, consider subscribing here.

Cloud Spending Growth Resumes in 2024

Global XaaS bookings dipped 11% during 2023. This was a sign of a maturing cloud market. By Q1 2024, around half of applications in G2000 enterprises had already been migrated to the cloud, and enterprise cloud priorities were shifting to AI. ISG predicts investments in AI will lift XaaS spending by 15% in the remaining quarters of 2024.

Data Watch

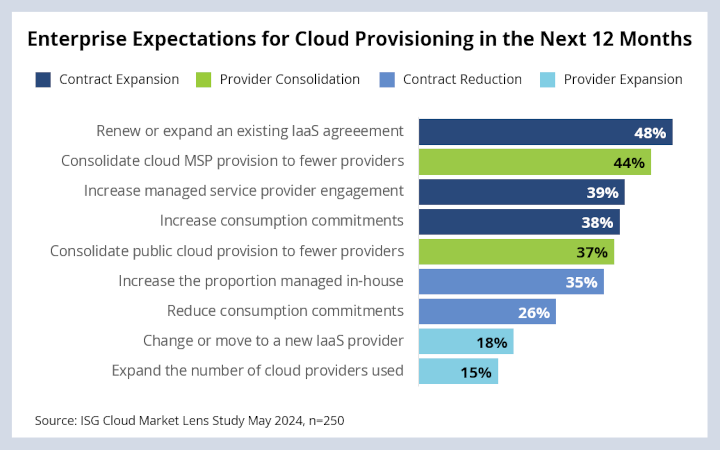

Background

In our AI Market Lens Study in January 2024, we found enterprises were planning to double their AI spending and that around 40% expected cloud spending to increase as a direct result. Most of these organizations built their cloud provider ecosystems before AI became a key priority in cloud strategies, so, not surprisingly, they are now re-evaluating their cloud provider strategies in light of these evolving needs.

The Details

- Between 2022 and 2024, the average number of public cloud providers used by large enterprises increased from 1.8 to 3.2, and the number of managed service providers supporting cloud services increased from 2.0 to 3.6.

- We may be close to the peak of multi-cloud, with the number of enterprises expecting to consolidate providers double that of those expecting to engage new ones.

- Growth in cloud services will accelerate in 2024. 43% of companies expect to expand cloud provisioning for existing AI capabilities and a third expect to add new graphics processing unit (GPU) provisioning for AI into their existing cloud contracts.

Some Providers Will Lose Out in the New Wave of Cloud Growth

Strong market growth for cloud spending and a lack of enterprise desire to engage new providers would be great news for incumbent providers were it not for the fact that 44% of enterprises expect to remove at least one cloud managed service provider in the next 12 months. Like we saw with megadeals, incumbency is both an advantage and a risk.

Providers most at risk will be those that fail to deliver expected value to businesses with their existing services or miss the mark in supporting new AI demand. Successful providers will need to differentiate as enterprises negotiate more aggressively, re-align and measure providers against their own business outcomes rather than solely against operational metrics.

About the author

Michael Dornan

Michael Dornan is a Principal Analyst in Provider Services based in the UK. He is responsible for ISG’s Buyer Behavior research program, helping providers navigate changing market dynamics, identify unmet enterprise demand, and position services and solutions that align to client needs.