Hello. This is Stanton Jones and Sunder Sarangan with what’s important in the IT and business services industry this week.

If someone forwarded you this briefing, consider subscribing here.

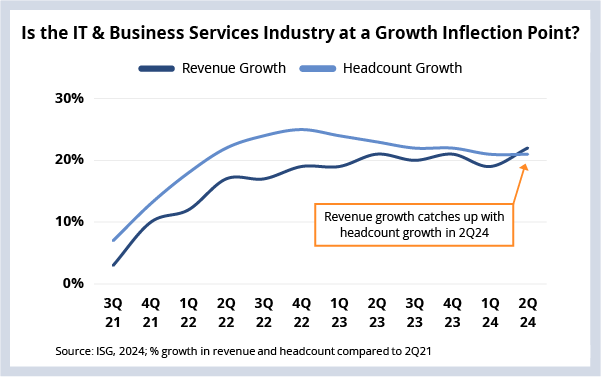

Growth & Hiring

The technology services industry is smaller by headcount compared to the end of 2022. But during the same six quarters, industry revenue grew. Is this a sign of non-linear growth?

Data Watch

Background

The IT and business services industry has generated six consecutive quarters of annual contract value (ACV) of $10 billion or more. But, even so, growth remains sluggish as discretionary spending slows the conversion of these bookings into revenue.

As a consequence, hiring in the sector is down significantly. There have now been six consecutive quarters of headcount declines in the industry. This means the industry is smaller today by headcount than it was at the end of 2022.

But something interesting happened this quarter. As you can see in this week’s Data Watch, cumulative revenue growth for the last three years caught up – and surpassed – the corresponding change in headcount growth.

The Details

- Headcount for the industry is now 3% smaller than its peak at the end of 2022.

- Since 2Q21, revenue across the industry is up 22% while headcount is up 21%.

What’s Next

Is this a signal that non-linear growth in the industry has finally arrived? We don’t think so.

While automation is having and will continue to have an impact on service delivery, it’s not responsible for this most recent inflection point. The benefit of predictive AI has already been factored into most contracts, and we’re just now starting to see the impact of generative AI and the downstream reduction in effort.

So why is this happening now?

Looking back at 2021-22, the industry saw unprecedented levels of revenue growth – and unprecedented levels of attrition. Providers ramped up hiring in a big way in anticipation of both continuing. However, growth started to slow in 2023, and hiring slowed to match. This combo, along with continued attrition, is why the industry is smaller today than it was two years ago.

So, revenue has finally caught up with headcount. The net result of this is that utilization levels are now up across the industry. This means the inflection point here is about providers’ delivery capacity rather than a sign of non-linear growth.

We do believe we’ll start to see hiring ramp back up. That may actually be starting to happen as 2Q24 saw the smallest decline in headcount in six quarters.

For ISG enterprise clients, it’s a good time to review the delivery readiness of your strategic outsourcing partners. It takes time for providers to ramp up hiring in response to a spike in demand, which can also trigger attrition, especially for in-demand skills.

About the authors

Stanton Jones

Stanton helps enterprise technology leaders, IT service providers and buy- and sell-side professionals make sense of the global IT services sector. Stanton's weekly briefing - the Index Insider - is read by thousands of industry stakeholders each week.