Hello. This is Stanton Jones and Owen Wheatley with your weekly briefing on what’s important in the IT and business services sector.

If someone forwarded you this briefing, sign up here to get the Index Insider every Friday.

BFSI

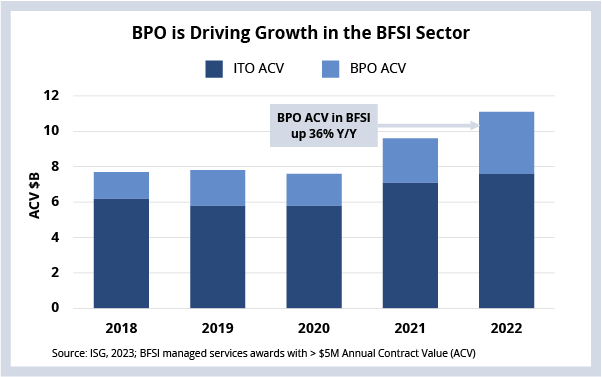

BPO is driving a significant portion of the record-setting growth in the BFSI sector.

Background

2022 was a banner year for the BFSI sector. Most providers saw record ACV levels as their clients doubled down on outsourcing to decrease costs, standardize processes and accelerate transformation.

However, most of the growth in BFSI ACV was in the middle office, rather than in IT. For example, retail and commercial banks are putting significant focus on transforming financial services operations (FSO). This includes things like core banking, lending and cash management.

This means that a lot of the growth from 2022 was in industry specific BPO, rather than in ITO. We saw this qualitatively with our clients as well - demand for traditional IT outsourcing or labor arbitrage based BPO was flat at best, while demand for services aimed at streamlining and transforming core operations surged.

But it’s not just managed services where financial services firms focused their transformation efforts. We also saw significant activity in other areas like FinTech partnerships, internal re-engineering, and of course, cloud.

The drivers for much of this activity remain the same: operational simplification, building new ecosystems of third-party providers, and a focus on employee experience to generate better ROI, increased productivity and – ultimately – improved customer experience.

The Details

- Record-setting managed services ACV of $11 billion was up 14% Y/Y.

- The lion’s share of that growth came from BPO, which was up 36% Y/Y.

- BFSI now makes up over a third of all managed services ACV.

What's Next

Market forces have complex and sometimes countervailing effects in the financial services industry - especially in retail and commercial banking. So, with the assumption that interest rates are likely to continue to go up in the US and in EMEA (at least in the short term) in order to tame inflation, some financial institutions will benefit more than others.

However, we believe cost optimization, especially within the middle office, will continue to be a big priority in 2023 as firms increasingly face margin pressures. Here’s why:

- Retail and commercial banks will see increased cash flow and net interest margin from higher interest rates. But lower consumer spending, combined with potential defaults, will likely cause a net negative impact on profits.

- Wealth managers, whose fees were already under pressure due to competition, technology-based new entrants and client mobility, are likely to see a decrease in performance-based fees given the performance of equity markets over the past six months.

- Insurance firms, already creaking under the weight of technical debt, will increasingly focus on cost optimization, given the fact that inflation is driving up costs, especially in the property and casualty sector.

- Investment banking receives a degree of natural insulation from volatility due to greater diversification of income streams, however, they are typically part of a larger bank where cost optimization very much applies.

So, while outsourcing demand will continue to be strong in sector for the balance of the year, providers with strong cost optimization propositions, in addition to more transformative services focused on financial services operations, will be set to capture the bulk of the demand in 2023.

DATA WATCH

About the author

Stanton Jones

Stanton helps enterprise technology leaders, IT service providers and buy- and sell-side professionals make sense of the global IT services sector. Stanton's weekly briefing - the Index Insider - is read by thousands of industry stakeholders each week.